Risk · Compliance · 2026

Pool Insurance in South Africa — What's Covered vs What's Not

Most South African homeowners assume their swimming pool is automatically and fully covered by their buildings policy. The reality is more nuanced — the shell, fixed equipment and public liability are insurable, but a long list of wear-and-tear and compliance-conditional exclusions trip up claims every year. This guide breaks down what to expect across major short-term insurers, where the boundaries sit, and which compliance steps materially change a claim's outcome.

Typically covered

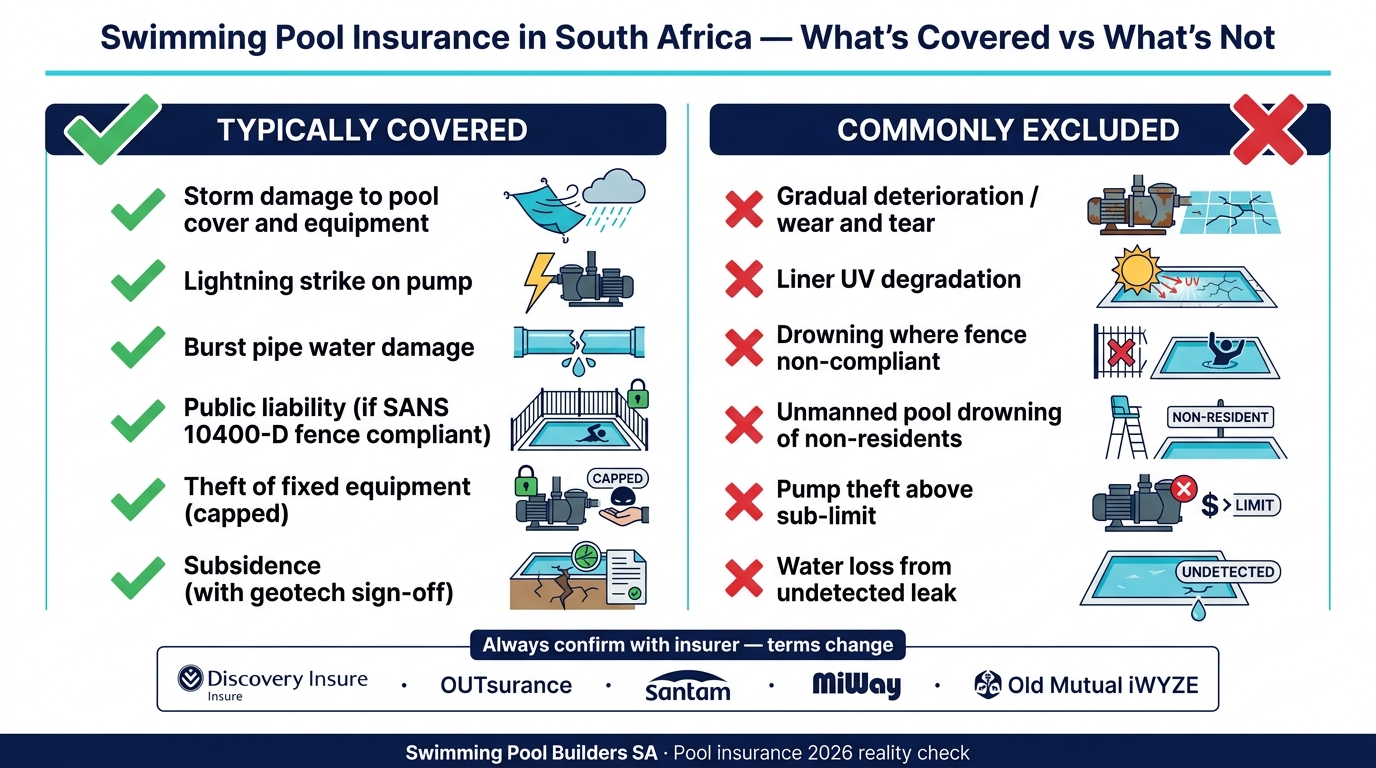

- Storm damage to pool cover and equipment

Hail, wind and lightning damage to slatted covers, thermal blankets and exposed pumps are typically covered as part of the buildings section.

- Lightning strike on pump or chlorinator

Surge damage to electrical pool equipment is generally covered, often with a per-item sub-limit. A surge-protection device on the pool DB strengthens any claim.

- Burst-pipe water damage

Sudden bursts in pool plumbing or supply lines causing structural water damage are usually covered. Slow leaks are not.

- Public liability (if SANS 10400-D fence compliant)

Third-party injury claims are covered where the pool meets SANS 10400-D safety barrier requirements. Non-compliance is the single most common reason a liability claim is repudiated.

- Theft of fixed equipment (capped)

Pumps, salt chlorinators and motorised covers fixed to the property are insured against theft, typically up to a sub-limit of R15,000–R40,000 per item.

- Subsidence (with geotech sign-off)

Foundation movement and subsidence on the pool shell are insurable where a registered engineer's geotech sign-off exists at policy inception — especially in dolomite and expansive-clay zones.

Commonly excluded

- Gradual deterioration and wear and tear

Marbelite cracking, gel-coat fading, tile delamination and pump bearings failing from age are excluded. This is the largest single exclusion category.

- Liner UV degradation

Vinyl liners cracking or fading from sun exposure are treated as wear and tear, not insurable damage.

- Drowning where the pool fence is non-compliant

A liability claim for drowning at a pool without a compliant SANS 10400-D barrier is almost universally repudiated.

- Unmanned-pool drownings of non-residents

Trespassers and unsupervised visitors are excluded under most public liability sections — explicit invitation and supervision are required.

- Pump theft above the sub-limit

Where the equipment sub-limit is R20,000 and a R35,000 pump is stolen, the policy pays only up to the sub-limit. Schedule high-value equipment specifically.

- Water loss from undetected leaks

Slow water loss through cracked plumbing or shell movement is excluded unless a sudden burst is demonstrable. Municipal water bills from leaks are not reimbursable.

Frequently Asked Questions

This guide is independent editorial content and does not constitute financial or insurance advice. Confirm exact wording with your insurer or broker — policy terms always supersede any general guide. See our editorial standards.